Flipkart Pay Later

Building consumer finance products for next half billion internet users.

After the successful launch of the Flipkart’s co-branded credit card, I set my eyes on another consumer finance offering - Flipkart Pay Later, a payment method that allows consumers to pay for their purchases on the platform at a later date. This payment option was designed to make it easier for consumers, particularly those from tier-2 cities and beyond, to purchase products on Flipkart, especially if they don't have the funds available to pay for their purchases upfront.

While the Indian e-commerce industry was growing rapidly, leading to a surge in credit consumption, this created a lucrative opportunity for disruption as the demand for such products was already strong. To meet the growing demand, micro-consumer durable loans products such as Flipkart Pay Later have come to the forefront, offering customers the chance to purchase high-end products at zero interest rates. This changed the landscape of credit consumption and pushed consumers to choose products of a higher grade than they would have aspired to previously. With the introduction of these products, customers have been able to access a range of items that they may have previously not been able to purchase due to financial constraints. Moreover, these products have also allowed customers to spread their payments over a longer period of time, making it easier for them to manage their finances. The growth of micro-consumer durable loans products is thus a major driving force behind the increasing adoption of credit consumption in India.

While leading the product design for our lending products such as Pay Later, Advanz EMIs, and a new strategic initiative Advanz app, I had the opportunity to work on a variety of projects to reach more customers and scale across their journey from customer acquisition, underwriting, disbursement, to repayments. Our product team (product managers, user researchers, and I) also traveled to Delhi and Bareilly for a foundational study to gain an in-depth understanding of the experiences of people in these emerging Indian cities with loan applications and banking. Even after having lived most of my life in India, I was astonished to discover the considerable differences between the lifestyles and problems faced by people in these cities versus those of early internet adopters in tier-1 cities. The latter are the driving force behind India's growth and development in the next decade and beyond. Consequently, it was important for us to gain a thorough understanding of the needs of people in these emerging markets, their preferences, and the problems they face in their day-to-day lives. With this knowledge, we headed back to design the Advanz App that was tailored to their unique requirements and help them progress and benefit from the advancements in financial technology.

My efforts, in collaboration with the amazing product managers, engineers, and marketers I partnered with, paid off, as we managed to acquire 1 million+ customers on Flipkart Pay Later and increased its checkout adoption rate from 7% to 18% during my tenure. During my time working on various facets of this product, I was also able to take part in design workshops, evangelize the new product line to Flipkart’s leadership, scale design operations within the team, and receive product management mentorship from my product group’s GPM. All these experiences have allowed me to gain an in-depth understanding of the problem space and build skin in the game.

Flipkart & Fintech

Scaling affordability constructs such as Flipkart Pay Later was of prime importance to us for a couple of reasons.

- 1. 15% of all Flipkart GMV comes from a form of affordability and is expected to go to 35% in just the next four years. This is critical as it not only increases the ASP (Average Selling Price) by 46%, but also the TPC (Transactions per Customer) by 40%.

Therefore aligning with the Flipkart and Payment Group goal of driving consumption of commerce on Flipkart platform, measured through Units Sale, GMV (Gross Merchandise Value), and TPC (Transactions per Customer); and

Since its launch, Pay Later has 1 million adopters and they contribute to ~3% of transactions today (as of 2020). An interesting statistic that has come to light is that a Pay Later adopter shows 65% stickiness to the instrument and 80% more TPC. - 2. Globally, Internet companies with high distribution and user data - both payments and non-payments had emerged as leaders, and this was been seen even closer to home. In fact, 344 Fintech startups have raised $3Bn to pursue this goal, many of them trying to build bottom-top Fintech intelligence. This has meant that customers have a lot more options at their disposal to make their purchases more affordable, allowing them to enjoy the products and services they need without having to break the bank.

To successfully implement this payment instrument, we had to address a number of challenges, including,

- 1. Increasing credit coverage as more than 50% of our customers were "New To Credit". New to credit customers are individuals who have never had any experience with borrowing money or using credit products. They may not have a credit history, or may have a limited credit history, and as a result, may be considered a higher risk by lenders. These customers may face challenges in accessing credit products, such as loans or credit cards, and may have to pay higher interest rates or fees. They may also be less familiar with how credit products work and may need more education and support in order to use them effectively.

- 2. Making customer acquisition simple and credit disbursement faster than ever - verifying the identities of our customers with our robust KYC suite including cKYC, XML KYC and eKYC. Assessing their creditworthiness, ability to repay their debts, and managing repayments effectively.

- 3. Lastly, we also worked on increasing the checkout adoption of Flipkart Pay Later. Making Flipkart Pay Later bigger than credit card transactions on certain categories like Lifestyle on Flipkart.

By utilizing Data, Distribution, and Technology in a scalable and efficient way, we can build a cash cow by outsourcing our capabilities to the wider ecosystem and leading to greater success of our products. This will ensure that our products will reach their peak performance and create the desired business results that we hope for. Furthermore, this will also have the positive effect of increasing our competitive edge in the marketplace, as we can focus on innovating and creating more value for our consumers.

Fintech Landscape in India

The global FinTech ecosystem is growing at a remarkable rate, with hundreds of new startups being founded each month across the globe. The US has been the leading destination for home-grown FinTech startups, topping the list for global venture capital (VC) funding every year. Between 2010 and 2015, the US saw 2003 FinTech startups launch, the highest number of any country in the world. However, India has recently made a surge, emerging as one of the fastest-growing FinTech hubs. India is firmly positioning itself as an attractive destination for FinTech investors and entrepreneurs, supported by a strong base of talented professionals and an abundance of capital. This is evidenced by the rapid growth in the number of FinTech startups being founded in the country, with many of them backed by high-profile venture capitalists. Moreover, the Indian government has also been proactive in its support of FinTech, introducing initiatives such as the Digital India program, which has helped to accelerate the growth of the sector. With its impressive growth trajectory and potential, India is set to be a major player in the global FinTech ecosystem in the years to come.

Digital lending FinTechs are targeting the unmet demand from Indian MSMEs as well as consumers for credit. Many banks in India have so far focused on highly creditworthy segments primarily due to a lack of credit history of others. The traditional ways of banking approve only ~25 to 40% of the loan applications. However, with access to alternate data such as transaction, behavior, app-based data, location information, social data from Indian’s leading consumer companies such as Flipkart, Bank are utilsing it for credit scoring , and more, these new lending models aim to increase this threshold by an additional 10–15%, which is a huge market opportunity.

From a small segment a few years ago, India now has over 338 lending startups. In consumer credit, the urban population is likely to leverage FinTech lending services to avoid heavy documentation. The rural population (which is new to credit) can benefit from alternative credit scoring mechanisms to avoid loan sharks. This would provide access to a market with over 300 million unbanked households. Hence, the use of identity, authentication, credit score, job eligibility, and social data to generate ratings for various use cases has drawn more attention to this space.

Like companies in other major industries moving to digital, traditional lenders are hoping to appeal to the new customers need to provide a viable online application process - especially when trying to attract younger borrowers. These younger borrowers of today have grown up in a world where technology is a part of their everyday lives, and they have come to expect streamlined, fast, and user-friendly experiences when it comes to financial services. The younger borrowers of today will become the majority segment of the market tomorrow, making it now imperative for the lenders to provide the kind of experience that these customers have come to expect.

To help with the shift, lenders may wish to consider partnering with some of the new entrants to consumer finance, such as the likes of Flipkart, many of whom have attractive customer experience propositions but lack the customer base or brand presence of traditional lenders. By forming strategic partnerships, traditional lenders can tap into the growing customer base of these new-age digital companies, while they in turn benefit from the brand recognition, trust, and infrastructure of the established players. This could result in a win-win situation for both parties, allowing them to combine their respective strengths and create a more seamless and efficient system for their customers.

FinTech Players

FinTech players have embraced the challenge of working towards financial inclusion and are facilitating the rapid adoption of financial services such as P2P mobile payments, alternative lending to small businesses & consumers, and more. Quite a few startups have emerged in this space, such as Jai Kisan, which empowers farmers through agri-credit; GramCover, which offers insurance for rural India; Kaarva, a credit line for regular income workers; Lakshya, which is working on improving the financial health of the urban underserved, and more. These, along with the traditional players, such as Paytm, PhonePe, and Lendingkart, will play a crucial role in ensuring that financial services reach every citizen of the country.

Fintechs have presence at every stage of the customers’ digital recourse

“India is larger than the world” - Foundational Research

Immensity of Indian culture and language with a quote from the Argentine writer Jorge Luis Borges

In late 2019, when I had just joined the team, Flipkart had two affordability payment instruments available: Pay Later and Cardless Card (Easy Monthly Installments, EMI). We were trying to restrategize our consumer finance offering based on the learning we had gained over the 1.5 years since launching these products. Due to ever-changing fintech regulations, we knew we needed a suite of expandable product offerings to move us from Business Continuity Plan (BCP) mode and allow us to think about our product with a long-term vision.

As I continued to work on various elements of the existing product, laying the foundation blocks in place for a robust future, I also collaborated with the product managers to craft the product strategy vision. After we had a concrete strategy based on our learning from the past, the market landscape, customer verbatim, and initial executive buy-in, we conducted a foundational research study to validate our hypotheses.

Our product team (product managers, user researchers, and I) also traveled to Delhi and Bareilly for a foundational study to gain an in-depth understanding of the experiences of people in these emerging Indian cities with loan applications and banking. Even after having lived most of my life in India, I was astonished to discover the considerable differences between the lifestyles and problems faced by people in these cities versus those of early internet adopters in tier-1 cities. The latter are the driving force behind India's growth and development in the next decade and beyond. Consequently, it was important for us to gain a thorough understanding of the needs of people in these emerging markets, their preferences, and the problems they face in their day-to-day lives. With this knowledge, we headed back to design the Advanz App that was tailored to their unique requirements and help them progress and benefit from the advancements in financial technology.

During our research, we sought to understand various aspects of our participants' relationship with money, particularly their need for a loan, from the beginning—why they needed the loan, their loan application journey if they had applied for a loan in the past, and the various use cases for loaned money.

We conducted our research in both a tier-1 city (Delhi) and a tier-2 city (Bareilly), giving us a good variety of needs and the problems our participants faced. Our participants included tech-savvy youth, a farmer, a customer support agent, a gym owner, and a student, all aged 25 to 35.

Key Takeaways

1. No Money during Medical Emergency - This was a common need that was surfaced across both the cities in which we interviewed. Many participants in the past had applied for a loan to fund the expenses for medical emergency of a family member, but were often unable to secure the necessary funds in a timely manner. This was a major issue that was highlighted by many of the participants during our interviews, and it was clear that the lack of financial resources available to them was a major source of stress and anxiety. In order to tackle this problem, some of our participants suggested that the government should provide incentives for financial institutions to provide loans to those facing medical emergencies, in order to ensure that they are able to receive the necessary funds in a timely manner and not have to worry about a lack of financial resources.

2. Borrowing Money from relatives is a social obligation - Many participants who had previously been rejected for a loan from the bank almost always felt the need to borrow money from their relatives, in spite of the potential consequences. This often meant that a family member was putting their financial state on display to others, which was usually frowned upon and resulted in a loss of social capital. Moreover, the need to borrow money from relatives has become part of the social fabric of many cultures, as it is seen as a way of honoring prior commitments and respecting the familial bonds that exist between family members.

3. Zero Savings, Always overshooting the monthly budget - Some of our participants were single breadwinners for a family of retired parents, housewives and children, and their monthly expenses always overshot the available budget. They mentioned that even a loan amount of ₹5,000-₹6,000 (~$70) could be immensely supportive, particularly as a buffer towards the end of the month, alleviating some of the strain on their finances and allowing them to spread out their purchases over a longer period of time. This extra buffer could help to ensure that the budget is not overrun, and help these families to avoid the financial strain that comes with overspending.

Workshops and Meet-ups

Women in Product and Flipkart got together a diverse group of product managers, designers, and engineers to talk about the importance of product management and learn about the challenges of building products that satisfy the unique needs and demands of a young and tech-savvy India. This workshop was an opportunity to bring together individuals from various backgrounds, experiences, and perspectives, to collaborate and work towards understanding the nuances of the problem statement.

Tejasvita, a product manager I was working with, and I partnered together to conduct a workshop during this event. Our goal was to work with fintech enthusiasts and help them learn about the problems in making fintech products accessible for a diverse set of users with various demographics, socio-economic backgrounds, and behavioral patterns. The challenge we put forward to the participants was:

How can we create digital experiences that build trust and make financial services accessible and simpler in an Indian context?

We wanted the participants to understand the target audience for whom they would be solving the challenge and to immerse the audience's mindset to think in terms of trust and accessibility in their context. To do this, we provided them with two user personas to help them better conceptualize the problem.

The teams were then tasked to design innovative yet practical experiences that explained how to bring trust and accessibility in fintech products, thereby contributing to financial inclusion. Tejasvita and I, as the facilitators, set brainstorming rules and introduced the teams to sketching ideas. Each team worked on a presentation to paper presentation, telling the story of their solutions and receiving feedback from us at the end of the day.

This workshop was especially enlightening for me, primarily because it was my first public workshop that I had organized. It was an opportunity to meet fellow builders who were passionate about the problem statement, and to witness the expression of daring ideas that can potentially shape the future of one's work. It was an empowering experience to see the immense potential of collaboration between individuals from various backgrounds.

Read the story here - The workshop truly opened my eyes to the possibilities of creative problem-solving and I am grateful for the opportunity to have been a part of it.

While deliberating on our Advanz App strategy, the entire working group also attended a workshop by TTC Labs (Trust, Transparency, and Control Labs from Facebook). It had been hosting a series of Design Jams in India under the theme “Design for Bharat” and this was the third design jam in this series that was hosted in Bangalore. During the workshop, we got together and worked with numerous other startups in Bangalore that were operating in the fintech space, and the focus was on targeting the ‘next-billion’ customer cohort in India. The workshop was filled with various group activities and discussions, and it was a great opportunity for our team to gain new ideas and inspiration from others on how different teams were thinking about similar problems. It was also a great opportunity to network and build relationships with other startups, as we discussed and debated the various strategies and solutions that could be used to address the needs of this customer cohort. Overall, the experience was an eye-opener, and it was a great learning experience for us, as we explored the growing possibilities in the fintech space in India.

Broader View into the Next Billion Users

A billion new people are expected to come online in the next couple of years, and it's estimated that almost all of these new users will gain access through a mobile phone. This is due to a combination of factors, including decreased costs of smartphone production, shifting localities for labor, increased rollout of Internet pipes, and an aspirational desire for access to the world wide web.

Nowadays, thanks to advances in technology, Internet-based software can be made available to millions of people in a rapid and efficient manner, with access to the web becoming increasingly ubiquitous in many parts of the world. However, it's important to note that technologies entering these different cultural, social, and economic contexts often need to be designed with an understanding of the practices, values, and infrastructures of each area.

The technology community can play a crucial role in this process, bringing a much-needed insight into the design process and helping to ensure that the technologies are implemented in a manner that's best suited to the local context. Here is a consolidated view to how the emerging market’s behaviors online:

Discovery

The contents and scale of the internet are a black box that many new internet users are not familiar with, and as a result, they are unaware of the potential their smartphone offers them.

Offline app sharing is the go-to method for many new internet users, as it is easy and convenient to transfer apps or media “offline” through SD cards, bluetooth, and file sharing apps. While this is a great way to discover new apps or media, it does not allow for exploration of what else is available on the internet, and limits the ability to receive routine updates. This means that the user is missing out on the full potential of their device.

Although offline app sharing is a great way to discover new apps and media, it is important for new internet users to make use of online resources, such as search engines and online communities, to ensure they are making the most of their smartphone. This will help to ensure that they are not missing out on any potential opportunities offered by the internet, and that they are getting the most out of their device.

Support and Assistance

Asking for help can be a source of shame for many people. In certain circumstances, people may feel awkward, embarrassed, or ashamed to reach out for assistance, especially when the inquiry is related to something they believe should be “simple” such as using their own smartphone. It can be difficult navigating the online world, and it can be particularly confusing to know who (or what) to trust on the internet. New internet users have a hard time deciding who to turn to for help, as they have been relying on their ‘CTO’ friends, family, and neighbors for trustworthy advice their entire life. It can be disconcerting not knowing who to turn to when they are in need of assistance in the online world.

Digital Money

Digital currency feels less trustworthy than cash and this can be seen in the way that its lack of physical artifacts like receipt slips, passbooks, and ATM cards can stoke fear in early internet users that their money isn't safe, or that their transactions are not successful. Additionally, lack of financial literacy can prevent new internet users from engaging with digital financial services. This lack of knowledge may mean that they need to learn why saving money is important or what a loan interest is, before they can engage with these services. This can be a difficult task for some, as the digital world is a far cry from the traditional cash-based economy that many are accustomed to.

Accounts & Identity

The mental model of “account” can be confusing, particularly when people are used to having one identity in the offline world. It can be difficult to understand why one would need different accounts and email addresses for different services and platforms. For example, why would one need a Google account and email address to setup an Android phone, while a different service like Flipkart requires a separate account altogether?

Creating an account (and remembering the credentials) can be a difficult and overwhelming process. Many people may have difficulty remembering alphanumeric passwords, especially if the credentials were created by someone else (most likely someone who assisted them in onboarding to a service). This is even more challenging when one needs to manage multiple passwords. This complexity can leave new internet users feeling overwhelmed and confused.

Textual and Numerical Literacy

The internet of today is designed to be read, yet the barrier to entry is high for those who are not literate. This can be an especially daunting task for the more than 781 million non-literate adults in the world, who are unable to participate in the digital world. Even for those who are literate, the use of keyboards can present its own unique challenges. Typing can be a difficult task for those who lack the necessary literacy skills, and for those who speak languages with more characters, the task can be nearly impossible. This means that tasks such as adding a contact, which can be an essential part of the digital journey, can be failed, resulting in a loss of confidence. Ultimately, the lack of literacy skills can put a user at a major disadvantage in the digital world, and this is something that must be addressed.

Connectivity

Reliable internet connection is an edge case; not the norm. Even though this is proven to be solved to a large extent by the entry of Jio, many new internet users in India still find themselves disconnected from the internet for the majority of their time, whether that’s because there’s no connection available or they’re simply trying to conserve data. Even when they’re connected, it’s often flaky and unreliable. As a result, users often blame themselves for any broken connections or errors when using apps. When an app isn’t working, new internet users often assume it’s their fault, thinking they’ve pressed a wrong button or simply aren’t educated enough to use the device. This can be a major barrier to the adoption of the internet and its many services, as users become discouraged from using technology due to their lack of confidence in their own abilities.

Data Consumption

The cost of connecting to the internet is often prohibitive for many, making it difficult for many early adopters to access the digital space. Data is becoming cheaper in many parts of the world, but the associated cost of purchasing the necessary equipment to access the internet, such as a smartphone, is still high. This makes the cost of data consumption a major factor for many users, especially those who rely on prepaid data plans, where they have to purchase a fixed amount of data upfront and then budget their data use over time. This can be especially difficult when there’s a daily tradeoff between internet access and other necessities. Furthermore, data consumption is often opaque and uncontrollable, making it difficult to tell how much data apps and tasks will consume. This can be incredibly frustrating for new internet users.

Shared Devices and Privacy

Phones are constantly switching hands, raising serious questions about the safety of personal information and privacy. New internet users, especially those who share a device amongst family members, borrow a phone from a stranger, or have someone else perform interactions on their behalf, face an even greater risk when it comes to protecting their data.

Gender norms can also play a role in introducing new threats to personal privacy. For example, if a husband is inspecting his wife's phone, she may be less likely to use certain features or applications for fear of the consequences. In some cases, the lack of privacy may even influence the way someone uses the device in general. This is why it is so important to ensure that personal information stored on phones is safe and secure.

Onboarding

An app’s purpose isn't always apparent, and this can be especially true of apps that are preinstalled. Their origin is unknown, their function is mysterious, and the fact that they seem to be a permanent fixture can be incredibly frustrating. Those who are new to the internet can find applications through friends or family, but the onboarding information they receive is often either missing altogether or not comprehensive enough.

These difficulties can be further compounded for users who are low literate and not familiar with interaction patterns. If the onboarding process is too complicated, it can create a barrier that is too difficult to overcome. As a result, they may choose to abandon the flow completely, leading to a high drop-off rate. This can be a major issue for those who are new to the internet, as they may be unable to take advantage of the benefits of certain apps and services.

Language

Content is often not available in a user’s preferred language, and estimates say that web content is currently written in English more than 50% of the time, with Hindi, the fourth most widely spoken language in the world, not even appearing in the top thirty languages for web content. Even if content is translated into a new internet user’s preferred language, it is often of a very poor quality. Digitally switching between multiple languages can be a challenging task and this is especially true for new internet users who live in contexts where multiple languages such as regional and vernacular languages are spoken. While these users may be used to switching between languages in their everyday lives, it can sometimes be more difficult or even impossible to do so on their phones.

9 out of 10 new internet users in India are likely to be Indian language(vernacular) users. Source: Google-KPMG report published in 2017

Interaction Patterns

Knowing when and where to tap, swipe, and long press can be confusing for new internet users, especially with inconsistent interfaces across different apps and operating systems. This can often lead to users heading down incorrect pathways as they resort to trial and error to learn new interactions. Blind tapping can be a common issue, which can result in unfortunate outcomes. Moving through hierarchical structures is also a challenge, as these can be difficult for early internet users to understand and navigate. Flat screens can lead users to prefer linear navigation, and following complex nesting, deep hierarchy, and scrolling interfaces can be disorienting and counterintuitive for them as they move further into flows. Consequently, they may find themselves confused and lost, making it difficult to complete tasks.

Smartphone Anxiety

The fear of breaking, losing, or having a valuable smartphone stolen can be quite daunting. Acquiring one of these devices can be a costly investment, so it’s not surprising that new internet users feel overwhelmed and apprehensive about using their phones. This can lead to them being overly cautious when handling their phone, or even avoiding using it altogether.

The pressure to do everything “right” is often so high that it can keep new internet users from even attempting to complete a task. This is further reinforced when they witness other people effortlessly complete tasks without asking for assistance. It can be a discouraging experience for those who are just starting out and trying to learn how to use the internet.

Visual Language

An unfamiliar visual aesthetic can have a major impact on a user’s understanding of a user interface, as well as their willingness to interact with it. Visuals that don't take into consideration the local aesthetic can be confusing and seem out of place. For example, if a user from a rural village without a supermarket were to encounter an icon of a shopping cart, it likely wouldn't make sense to them.

Furthermore, visuals that are either too abstract or too detailed can be problematic for users. Abstraction can be seen as too vague and overwhelming, while excessively detailed visuals can be overly distracting and contain elements that are not relevant to the interface.

These behaviours open a can of worms especially for Interaction Designers. A plethora of questions have been lingering in my mind, such as:

What is the ideal design system for our users? How should the grid system be defined for India, where there is a culture of accepting imperfection and not expecting everything to go exactly as planned (Low Uncertainty Avoidance)?

Does this mean that imperfect, organic design is the next step for us? How can we manifest social trust online? What was the original intent of the early graphical user interfaces (GUI) that was analogous to our offline objects and behaviour? Why was there a skeumorphic celebration of design at one point?

At the end of the day, these are the types of questions we asked ourselves as advocates inspired by the cohort we serve —our next billion users. We wanted to ensure that we had taken into consideration the unique challenges and needs of this group, and that we had covered all of our bases to ensure that our design solutions would be successful.

Ghost Work

A lot of work that often goes into designing a product doesn't always make it to the public eye. These are often documents, Slack channels, brainstorming canvases where I spend a lot of time to get a better understanding of the problem. I look at competitors, stay up-to-date with the movements in the fintech industry, have brainstorming workshops with product managers, and prepare specifications for developers - all of which are critical parts of the process of delivering a valuable experience.

Efficient communication is essential for productive and satisfying relationships in the workplace. I practice what I preach.

Improving Processes and Fostering Collaboration

Look for ways to enhance the design workflow and collaborate with engineers and product managers to standardize processes.

Upholding Design Quality

Continually raise the quality bar by demonstrating solid craftsmanship, providing feedback, and actively participating in bug bash sessions for engineers.

Diagnosis, Insight, Action

I work with the team to identify problems and opportunities by analyzing insights and leveraging existing knowledge.Range of Problems Statements

While leading the product design for our lending products such as Pay Later, Advanz EMIs, and a new strategic initiative Advanz app, I had the opportunity to work on a variety of projects to reach more customers and scale across their journey, namely:

- 1. Customer Acquisition - Know Your Customer Module and KYC Upgrades

- 2. Underwriting - Alternate Date

- 3. Growth Initiatives - Externalization and Continuous Feedback

- 4. Repayments - Partial Payments

Always Know Your Customer

KYC is an essential prerequisite for extending credit line to any customer. There are several types of KYCs currently allowed by RBI (federal bank) which serve different use-cases.

One thing that stood out during my time building the KYC module was that, government regulations can play huge spoil sport in a product roadmap. There were times when we had complete shut down our new applications because we weren’t be compliant with the new regulations that the federal bank released for fintechs operating in the lending space. The only solution to this problem was to build a robout suite of KYC methods.

With KYC being a necessary part of the onboarding journey, the choice of KYC mode(s) should balance customer experience with a long-term view of business continuity and our ability to extend additional products to the customer without incurring additional friction in the upgrade path.

Traditionally were onboarding customer using the eKYC method but eKYC was not giving a great conversion funnel, xml KYC becomes the only Full KYC solution that we currently have. However, the same is relatively new and there is no formal circular from RBI/UIDAI that validates it as a full KYC in non-F2F mode. On the other hand, cKYC can be accessed readily by RBI regulated entities and treated as full KYC. Making it our first choice ensures that we are covered from a business continuity perspective, in case RBI places any restrictions on xml KYC in future.

Why XML-Based KYC?

XML-Based KYC Features

I collaborated closely with my product manager to create a well-designed user flow for customers. We conducted an extensive review of the types of KYC that were existing in the market, considering factors such as lender applicability, validity, user experience, transferability, and potential limitation. After weighing our options, we intelligently made these different modes into separate, modular building blocks to remain in compliance with ever-changing regulations. This approach proved to be highly beneficial, as it enabled us to route customers to the appropriate paths with minimal effort.

XML-based KYC is one of the most challenging pieces of UI I have designed primarily because of the technology constraints it involves. Since the government did not provide any API for utilising its XML-based verification, we had to figure out a way to extract the information being transmitted to the government servers and then send that across to our lender (IDFC Bank). For this, I had to design an assistive interface on top of an existing government website. The assistive interface was required to be contained in a web-view on which the government website was opened up. Moreover, the XML-file which carried the secret verification address for the individual applicant required a 4-digit PIN to lock it for security purposes.

Now, since this XML-module was built by the government as a mode of offline KYC, where the customer would save this XML on their device and physically transfer it to their bank unlocking it with the 4-digit PIN - meant that this particular layer of security served no purpose in our way of operation. I had long discussions with the legal and product managers to see if there was a way to bypass this particular field, but it turned out that we were not ready to take that risk since it could potentially lead to strict government bans. Even though this left us with little room for creativity, I did extend my ideas to utilizing an emoji passcode or captcha-like unique entry, but they couldn't make their way to the release. This project taught me an important lesson in creative problem solving and the lens through which legal teams view a product solution, as well as the importance of considering the security risks associated with any technological implementation.

KYC Upgrade

Most of the Pay Later users till now have been onboarded using eKYC, which is only valid for a period of 12 months and cannot be extended again. Thus, a significant chunk of users were starting to have their KYC expired and won’t be able to use Flipkart Pay Later further.

It is crucial to be noted here the timeline during which this expiry was starting was, Sep - Nov the most important calendar months for Flipkart Pay Later from a business perspective, which is also when we have our flagship sales event - The Big Billion Days.

This piece of Flipkart Pay Later was a long over due in term of customer verabim. Often times due to KYX epiry customers would comes calling to your CX respresentative on why their Pay Later option had suddenly been disabled. With no communications and representation of KYC method it was inevitable that we solve for this use case.

Even though wrapping the problem in my head was easy, it was difficult on how we would to draw a consequences to how we might position this feature. I went extremely broad during my solutioning phase because comprehending the comparison between the two KYCs was a major challenge.

Problems to be Solved

- 1. Does the user comprehend the comparison between the two KYCs?

- 2. Does the user, comprehend, that Minimum KYC is already done and they can continue to use Pay Later till another year?

- 3. Does the user, need to know what’s next before opting to upgrade?

- 4. Do we need to hint at the task load associated with Upgrade?

- 5. Are users confusing their Pay Later limit with 60k of KYC?

Since KYC was essentially a function of time (ie. time to expiry) and premissible usage limit. We took these two parameters and segmented the user into three buckets:

This helped us in constructing a flow that would help and progressively disclose the information on the KYC upgrade state and disseminate the information to the users. We knew that the probability of upgrade a KYC method was going to be highest for customer in the Amber and Red cohort so we designed nudges with variating intensity. Green cohort had no explicit nudge, Amber had a soft nudge and Red hard nudge that would force users into an upgrade path, ie doing their Full KYC.

Growth - Externalization

By utilizing Data, Distribution, and Technology in a scalable and efficient way, we wanted to build a cash cow by externalizing our capabilities to the wider ecosystem and leading to greater success of our products. This would ensure that our products will reach their peak performance and create the desired business results that we hope for.

Externalizing Flipkart Pay Later meant that customers could now start using their credit line on other partner merchants such as Myntra, PhonePe and MakemyTrip. This externalizing of Pay Later opened up more opportunities for customers to use their limit, something which stood out in most conversations with our users and hence increased the value proposition of the product for the customer. For Merchants, it meant the easy checkout solution such as ours would offer them Higher conversions and Higher GMV due to trade up by customers and hence increased conversions. In addition, for Flipkart, it gives us the ability to strengthen our credit model using transaction data from merchants (e.g. recharge data, utility bills data from PhonePe, travel related data from MakemyTrip). Moreover, it would lead to Higher Adoption (# of transactions) for pay later, thereby driving higher credit utilization and also commission from Merchant. Lastly, this would also help to create better customer experiences and loyalty which could lead to more customers joining and using the Pay Later service.

This was the first project that introduced me to the world of Buy Now, Pay Later (BNPL). I had to design a framework for the transactional. It was crucial that I incorporated all usecases sucha as forward transaction, reverse transactions and second-order transaction for mini-apps that were being served on the PhonePe superapp. Merchants are usually very cautious about providing transaction level details to third party to avoid leakage of their sales data and to avoid them from profiling their customers. Thus the framework I designed had to consider this varing modality. One of the problems that this created was because most customers were so used to being anchored to the order item names, now having to display the transaction without and order details was going to be difficult for them especially when they would see the bill towards the end of the month.

To solve this problem I had suggested two inputs:

- 1. Addition of Help and Support - which would help customers direct queries on a transactional level if they needed to.

- 2. Delinking Apps - Since we knew the cockpit was only going to available to customers on Flipkart. I had suggested we reserve a real estate in the cockpit for Linked Apps. This served would serve users with the ability to delinking connected merchants anytime they wanted to and provide them with greater control of their payment instrustment from and risk perspective.

A Resilient Tomorrow - Trusting Social

Finding the Cracks in Financial Service’s Trust Crisis

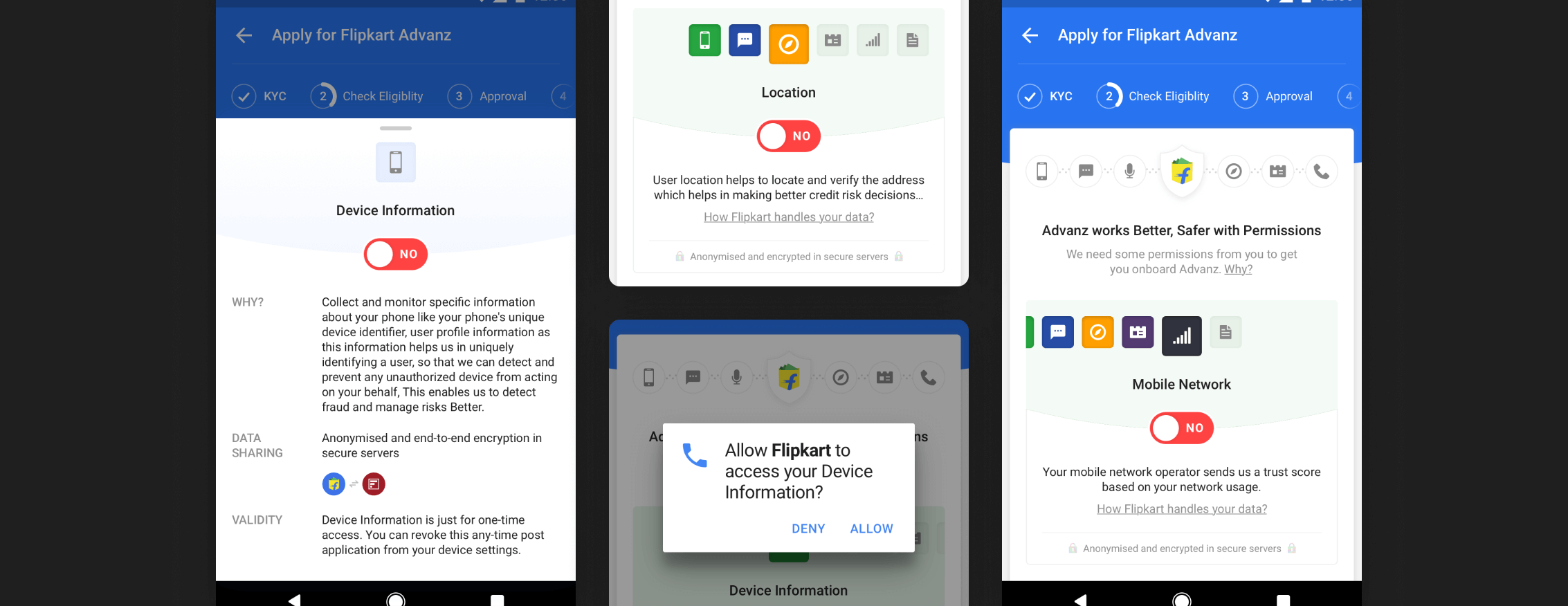

To achieve its objective of expanding access to Flipkart Pay Later to all Flipkart customers. Flipkart fintech needs alternative data sources to determine the eligibility of a user for credit. Current whitelist had a very small coverage into credit under-penetrated user cohorts - Cash on Delivery (COD) and Pre-Paid (Credit card, Debit card, Net Banking, UPI) users.

To achieve this goal we had partnered with Trusting Social to provide us with additional data apart from our available data on Flipkart platform. Trusting Social is an innovative South East Asian company that offers a unique way of determining a user’s credit worthiness. Through the use of telecom data, Trusting Social has made great progress in underwriting customers in countries such as Vietnam, where traditional credit scores such as CIBIL score are not accessible. The Trusting Social Score is used as a reliable signal for underwriting customers who do not have access to traditional credit scores, making it an invaluable tool for those in under-penetrated markets. This technology is helping to expand access to credit and make finance more inclusive for those who need it most.

Prior to using Trustingsocial, our credit model utilized various device inputs such as Device Information, SMS, Location, Contacts, and Bureau to underwrite users and assign a risk parameter to them. The image below depicts some of the insights that our data science team could derive about a customer based on these levers. Having seen this, I could understand how data is being used to allocate loans to customers in the emerging markets, and I was initially taken aback by this.

We had been underwriting customers based on SMS, Location, Contacts, and Bureau for over a year, and yet, I had never heard any negative customer verbatim in any of the meetings. This made me curious as to why this was the case, and I decided to open an investigation into the matter. Upon further investigation, I realized that privacy in today's world comes at a cost, and a cost that nobody in the emerging markets is willing to bear. Our customer, who had not yet realized the potential of their data and the value it could bring, was willing to unconsiously trade it away for the prospect of a sachet loan and a more comfortable lifestyle.

Consent Framework

India is going through a data revolution, as more people come online, an explosion of consumer behavior data is being generated. Startups in India, particularly those which are not only building for the urban/metropolitan audience, have the additional challenge of educating before innovating. While innovation is essential for creating compelling and valuable services, we cannot downplay the importance of educating the user on how their data is being used; this helps to build trust between them and the business. To further this idea of privacy and trust with our product group, I designed group working sessions which would help everyone identify the need to start thinking about alternate data input through this lens. To carry out this endeavor, I worked closely with the business team and product manager to better understand how users' data was being utilized and how customers who are being directed towards alternate data methods can be made aware of the data being collected about them, as well as the potential impacts of that data.

I designed a scalable framework that would serve the utility not just for the Trustingsocial project that we were doing, but also scale it up to incorporate Device Information, SMS, Location, Contacts, and Bureau data inputs. My goal for the Consent Framework was to make sure it was never perfect, but to keep the conversation alive and make it as meaningful as possible. To achieve this, I focused on making sure the framework was flexible enough to accommodate a wide range of use cases, even if they hadn't been fully foreseen. Additionally, I worked on making sure that there was an easy and intuitive way to access and adjust the framework, as well as making sure that it had the capability to be adapted to the changing needs of both the project and the users. As such, I went to great lengths to ensure that the framework was as comprehensive and accommodating as possible, while still being able to be used on the Trustingsocial project.

These were some of the questions that I was asking myself -

Does providing additional information such as a privacy rating improve consumer privacy decision making

Does reducing information change consumer understanding? Does presenting a summary ‘key facts statement’ improve consumer comprehension of the privacy policy?

Is there a willingness to accept for consumers to share different categories of data?

How do different levels of perceived control over personal information affect consumers’ willingness to share data?

Are consumers willing to pay to safeguard their shared data?

For the initial build up of this framework, we only piloted it with Trustingsocial, and we have continued to serve the remaining alternate data methods via the old designs. This is to monitor whether the open disclosures on the use of personal information impact consumers’ willingness to share data. We are particularly interested in how open disclosures can shape consumer attitudes towards data sharing and privacy, as well as how these attitudes might influence the types of data that consumers are willing to share. We are also monitoring the potential for open disclosures to influence the types of data that businesses are willing to collect and use. We believe that by understanding the impact of open disclosures, we can better design and implement data-driven products and services that protect consumer privacy.

Design is a team sport. I help translate business strategy into product roadmaps by facilitating collaborative, in-depth conversations with XFN, as well as liaison with engineers to design a great experience.

Here is a glimpse of some of the design thinking workshops I have led to uncover answers to challenging problems and inform product vision – ranging from design sprints to co-creation workshops, customer journey mapping, and more.

Customer Journey Mapping: Customer journey mapping exercise conducted for visualizing an end-to-end experience for TV Guide with XFN partners.

Purpose, Positioning, Placement: An example of a long term eco-system conversation with XFN, resulting in gaining alignment with the platform teams for our product integration.

Functional Framework: Define high level functional flows and map out data elements to help engineers in building the data schemas and app framework.

Monetizing Immediate Redressal - Partial Repayments

Next Billion Users are often accustomed to products that may not fit into their lifestyles or financial situations. Products that offer flexibility such as easy options to make up for missed payments, and convenience, can alleviate the burden of having to maintain rigid payment plans that may be hard to keep up with due to their income streams. Providing flexible such as Partial Repayment structures can help low-income consumers better manage their finances, and give them a sense of control over their spending.

Keeping convenience and customer needs in mind, Flipkart Pay Later has introduced Partial Payment as a way to provide customers with a flexible repayment option and extended credit period. This is a revolutionary offering that not only allows customers to better manage their cash flows, but also enhances the payback and collection experience. This is especially important in times of distress, when customers need more control over their finances.

Partial Payment was designed to empowering the customers to bring their credit needs and repayment terms under their own control, preventing them from getting over budget and giving a lifeline to the customers in situations of distress. A customer can avail this option on or before the due date by paying a minimum due amount (including convenience fee) to get the following benefits:

- 1. Extra credit period up to 30-days

- 2. No Late Payment charges

- 3. No collection reminders/calls

- 4. No negative reporting to the credit bureau Continued transactions on Pay Later account.

Partial Payment serves a two-pronged goal for Flipkart:

- 1. Making the Pay Later product self-sustainable through the monetization construct in the form of convenience fee charged to customers to avail this facility to extend the payback period of their outstanding bill and avail extra credit over and above the initial credit period

- 2. Ties back to the uber goal of improving affordability on the Flipkart platform by enabling the customers to manage unforeseen expenses using the credit construct. It also provides an opportunity to reward high payback intent and increase the trust of the customer on the platform.

Which metrics will be impacted?

Partial Payment capability for customers will lead to :

↑ Net GMV: expected incremental increase of 0.52% with a steady portfolio revolve rate of 15%

↑ NPS

Adoption So Far

- 1. ~5% users adopted the partial payment feature in the first two months of launch.

- 2. ~4.34% (13,829 unique customers) of all pre-due date billed transactions are Partial Payment transactions

- 3. Convenience fee collected so far: ~₹18,61,560. Avg amount paid using pre-due date partial payment: ~₹1,000

Next Steps

As next steps we wanted to experiment with the constructs like minimum due amount and convenience fee to evaluate their impact on customer adoption across risk cohorts to customize the experience for users and optimize monetization. We will analyze the potential risk shift in the behavior of customers from different risk cohorts after Partial Payment and assess the impact on metrics like NPA. Enabling Partial Payment for unbilled transactions.

Naye India ke Saath - Flipkart Advanz

Becoming the one-stop-shop for credit products and financial services for the aspirers and the next billion

By bringing together all the pieces of the puzzle we had been designing for the past year, Advanz App was an unique opportunity for me to build a product zero to one. All the smaller projects that I had worked on would readily come together to form this application. I was involved in this project right from the zeroth stage where I partnered with the Product Manager to lay the foundations to the product vision. This not only helped gain a macro view into the industry and its inner workings but also helped me gain experience in pitching our product to executives something I believe not many designers get such early on in their career. This experience taught me a great deal about navigating a workplace as large as Flipkart and build on my presentation skills.

The launch of Advanz started with the formation of a separate legal entity from Flipkart. This meant I was involved in its branding efforts with the marketing team as well. All my efforts into building more skin in the game by learning about the industry and were being paid off.

The timing of the foundational research study also help me gain a better understanding of our potential customers and validate the hypothesis with which I was operating on a day to day basis. This view allowed to be understand not just our product group’s principles and how it fitted in the overall goal of Flipkart but also other groups such as Design Systems team, Vernacular team, and Voice team, in the Flipkart that were building products for the same customer base.

Architecting the entire app from ground was herculean task, but I was well equipment the tools and relationships with my co-workers that I had honed from my prior projects.

As we were gaining momentum towards our goal of a full stack financial platform, it became increasingly apparent that checks and balances would be necessary for our design process in order to ensure that we are constantly considering the needs of our users. We believe that by taking the time to pause and refresh our perspective on our users, and reasserting their needs into every user story and decision we make, we can make sure that we are building a product that is tailored to their needs and interests. This mindful approach to design has become an integral part of our development process.

This collection of principles that we compiled and distilled from our research provides a meaningful context to our ongoing dialogue—with one another, with our users, with Bharat, and with what lies ahead in the future. The principles we have gathered unite us, guiding our conversations and giving them a sense of direction and clarity. We are confident that they will serve us well in our mission to continually improve the experiences we create.

COVID19

As dangerous as the situation with COVID-19 is, Flipkart unfortunately had to re-strategize many of its existing plans, while scaling up a few arms to address the new markets' needs. Some, such as Advanz, were deprioritized to focus on providing profitability from the existing capabilities that had already been built. Even though this shook the entire team's morale, we were glad to have had the opportunity to think and experience a vision as grand as Advanz. This incredible opportunity not only allowed me to grow as a designer, but it also made me develop as a professional. It provided me with a range of new skills and knowledge that I was able to apply in the workplace, while also teaching me how to work with different stakeholders and in different settings.

Reflection

Looking back, there are so many things I would have done differently on the project and the experience taught me so many lessons that have helped me to grow professionally.

Strategy is storytelling

I used to have conversations with my manager where I wasn't sure I was developing the skills I had expected before joining the team. I wanted to be the best designer, but my focus was limited to tools and problem-solving. It was only when I had the chance to work with the product team on strategy that I realized what else I could do. This experience taught me that it's not just about following the process – it's about understanding the problem, having an opinion on the outcomes and process, and taking the lead.

Skin in the game

Finance is a lovely industry, but financial investments are, by definition, incapable of reaching the last mile of human civilization; their business models simply don't work. To make our financial infrastructure inclusive of everyone, we need to start from scratch.

Gaining knowledge of an industry, understanding its workings, is as critical a skill in my toolkit as problem-solving. Industry knowledge is often overlooked, but I believe it is essential to the success of any design career and critical problem-solving skills. To this end, I created a Slack channel and Twitter list of people in the Indian Fintech space, and developed a personal stake in the game.

The key to leveling up isn't necessarily about learning new tools or frameworks. It's about becoming more informed about the world that surrounds your work. You're supposed to pour your life force into something, and it's not always supposed to be easy.

A well-oiled machine

During my project, I had the opportunity to be part of hiring panels for Flipkart's internships and full-time positions at India's top universities. I gained valuable insight into spotting talent and building teams.

Even if a company isn't scaling quickly, it's important to ensure new employees understand the culture, architecture, and ways of working. I was lucky to be a mentor for a few new designers, and while helping them onboard, I learned about unlocking talent. I also got to experience designOps first-hand, which I believe is one of the most underestimated functions in organizations.

To gel

One of the reasons I was able to extract so much from this project was because of the geniue curiosity of the people around me. I learned that, curiosity, often shown through asking great questions, is a powerful trait to build into team culture. As a creative, the questions we ask, the way you ask them, & forums we create for others to do the same is a powerful way of making it this cultural trait.

I learned that I can get a much deeper understanding of the ecosystem we’re in by spending time with stakeholders outside by direct working groups, such as marketing, growth and legal.

Zooming

We often become fixated on a solution when we encounter a problem. However, this solution may prove to be difficult or impossible due to a missing element. Consequently, we may spend valuable time attempting to fit the wrong piece into the puzzle. In reality, all we need is to adjust our perspective and recognize that there are alternative solutions that can solve the same problem quickly, with less effort and cost.

Special thanks to all the designers, engineers, and marketers who assisted me on this journey: Samir, Anurag, Rikkin, Sajal, Nuvena, Shivangi, Tejasvita, Ambuj, Anshul, Samiksha, KT, Ram, Prateek, Paras, Aditya.